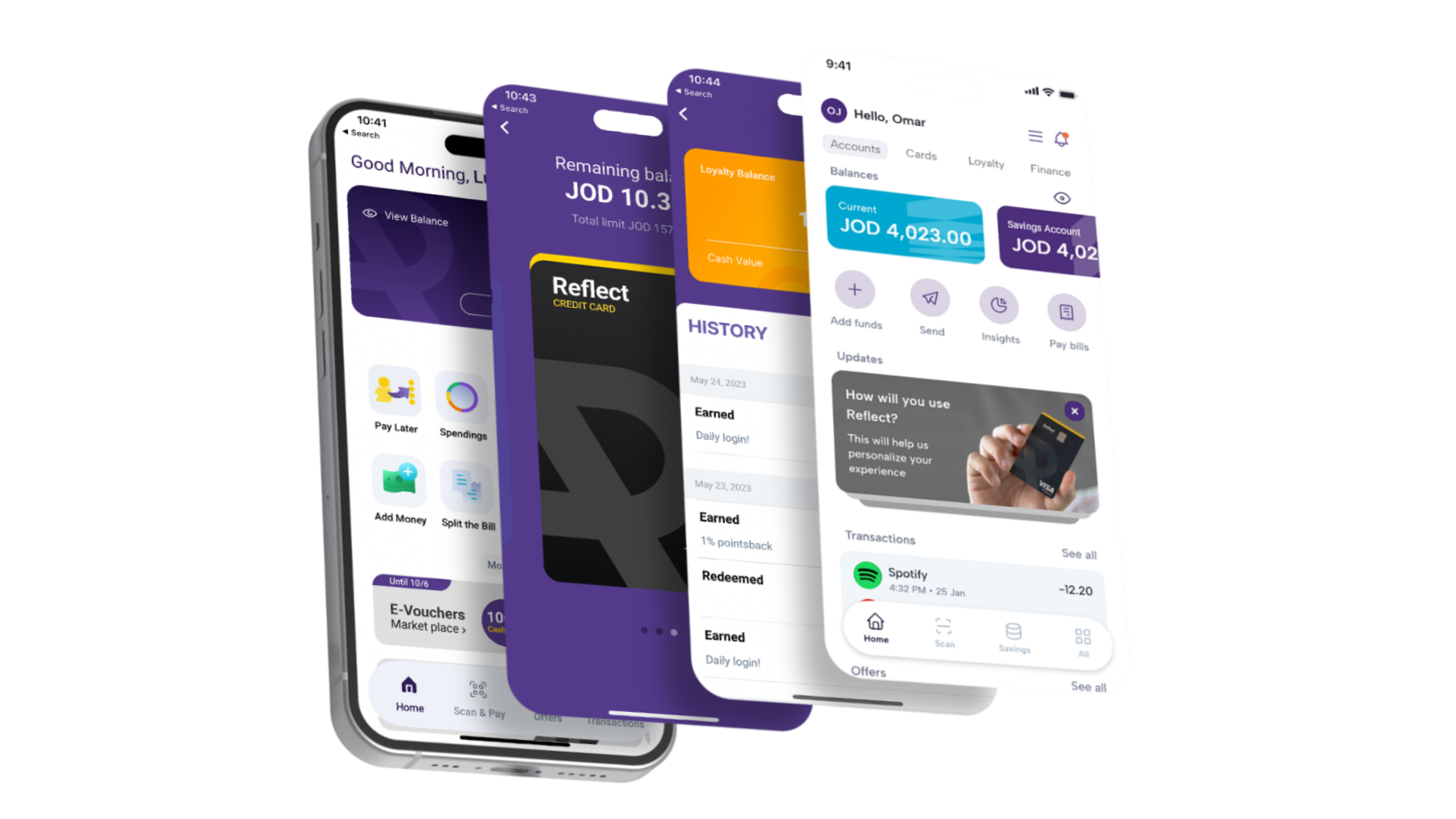

Reflect - Arab Bank

Product Strategy

Conversational AI

CX Design

Digital Banking

MACH Architecture

From measuring delivery to

building financial habits

A digital banking app with millions of downloads but no visibility into what customers did next. The solution was a product strategy, a measurement framework, and built-in AI integrations to close that gap.

Downloadable on iOS and Android

https://reflectapp.com/____________________________________________________________________________________________________________________________________________________________

ROLE

Head of Product and Growth

TEAM

Managed and mentored 6 product and UX designers

across research, product design, and delivery

TIMELINE

2023 - 2024

DISCIPLINES

Product Strategy · Service Design · CX Design · Growth ·

Conversational AI · Stakeholder Alignment · Facilitation

____________________________________________________________________________________________________________________________________________________________

CONTEXT

Jordan's first neobank built

inside a 100-year-old institution

Arab Bank launched Reflect as Jordan's first fully digital neobank. Commission-free, mobile-first, and built on MACH architecture (Microservices, API-first, Cloud Native, Headless). The product suite covered the full banking stack: wallet accounts, virtual and physical debit and credit cards, contactless payments, bill pay, savings accounts, BNPL, a marketplace, and a loyalty and rewards engine that drove daily engagement.

The strategic bet behind Reflect was about who it was built for. Arab Bank already had a strong regional foothold with wealth management clients and a dedicated youth product. Reflect was aimed at a different segment entirely; the mass consumer. People who were largely cash-dependent, working in trades and vocations, with irregular or informal incomes. People who didn't fully trust large financial institutions with their data, and who often couldn't access the main branches concentrated in capital cities.

For this segment, access was the core problem. A digital bank on their phone, requiring minimal documentation and built around a simple onboarding experience, wasn't just a better product, it was the only product that worked for how they actually lived. Getting Reflect right for this user wasn't optional. It was the entire premise.

Due to NDA and confidentiality constraints, some aspects of this work have been simplified or generalized.

Sensitive details and full client deliverables have been redacted. Additional details available upon request

____________________________________________________________________________________________________________________________________________________________

THE CHALLENGE

Everyone was measuring delivery.

Nobody was measuring habit.

0

Shared definition of what "success" meant post-download across Marketing, Product, and Leadership

0

Defined user archetypes grounding feature decisions in evidence of actual customer behavior

4

Separate teams each optimizing for a different metric -- none of which measured banking habit

When I joined, the team was building fast. Features were shipping on schedule. Downloads were climbing. Wallets were being created. On the surface, it looked like progress.

But when you looked at actual customer behavior, what users did after they downloaded the app, the picture changed. Marketing was optimizing for installs. Product was optimizing for releases. Leadership was optimizing for revenue. Each team was winning its own metric, and none of those metrics said anything about whether customers were building a banking habit.

The product was also untethered from any real understanding of who it was for. Features were built on assumptions rather than evidence. And with expansion plans accelerating, the cost of getting this wrong was multiplying.

____________________________________________________________________________________________________________________________________________________________

THE REFRAME

A strategy problem with design

implications downstream

Problem Framing

Core Problem

How do we shift Reflect from an app people download to a bank people actually use every day?

HMW 01

Build for banking habit, not just feature delivery?

HMW 02

Connect the right feature to the right user type?

HMW 03

Give all teams a single shared language for growth?

HMW 04

Make onboarding feel like the start of a relationship?

HMW 05

Surface behavioral signals teams can actually act on?

HMW 06

Design a north star metric that reflects real value?

HMW 07

Redesign support flows so customers self-resolve faster?

North Star

% of users with growing balances month over month

The main reframe was structural: we could not fix the product experience until we knew who we were building for, and we could not know if anything was working until we had a shared definition of success. This sequence mattered as much as the work to be done.

What Existed

- ›No shared metric for customer activation or habit formation

- ›No user personas grounding product decisions in evidence

- ›Onboarding built around feature delivery, not user intent

- ›Siloed teams each optimizing for a different number

- ›No behavioral intelligence layer connecting data to decisions

- ›Support flows that escalated rather than resolved

What We Built

- ›A North Star Metric tied to real banking behavior

- ›Four user archetypes grounded in behavioral and psychographic data

- ›A persona-aware onboarding flow built around user intent

- ›A shared strategic framework all teams could align to

- ›Funnel analytics, cohort segmentation, and social signal monitoring

- ›AI-powered chatbot with intent triage + in-app AI assistance; customer support resolution rate up 40%

____________________________________________________________________________________________________________________________________________________________

THE APPROACH

A four-pillar framework

built in sequence, each unlocking the next

The problem was structural, so the solution had to be too. I designed a strategic framework with four interlocking pillars. The order mattered because you can't redesign a customer experience before you know who the customer is, and you can't align teams around growth metrics before those teams have a shared vocabulary. Every pillar was intentional and sequential.

Pillar 01

Persona Development

Foundation for everything downstream. Defined four user archetypes along two behavioral dimensions - digital confidence and financial intent - giving every team a shared picture of who we were building for.

Pillar 02

CX and Onboarding Redesign

Rebuilt the end-to-end onboarding flow and support experience using journey maps, AI chatbot flow restructuring, and persona-aware messaging. The goal was to create a first experience that felt like the start of a real relationship.

Pillar 03

Ecosystem and Digital Intelligence

Built the behavioral intelligence layer: funnel analytics, behavioral cohort segmentation, and social signal monitoring. Designed the feedback architecture that routed behavioral signals back into product decisions. This is what turned data into decisions rather than reports.

Pillar 04

Cross-Functional Alignment

Ran co-creation workshops, established a shared KPI language, and advocated for a design system. Alignment was not a soft exercise, it was the infrastructure that made every other pillar stick.

____________________________________________________________________________________________________________________________________________________________

DESIGN ARTIFACT 01

User archetype matrix

Four archetypes mapped along two behavioral axes - Financial Intent and Digital Confidence. Built from behavioral and psychographic signals, not demographics alone. Became the shared language for roadmap prioritization and persona-matched onboarding.

User Archetype Matrix

Note: Many more personas may exist within each archetype based on demographics, behavior, and psychographics.

High Financial Intent

👩

Deal Seeker

High intent, lower confidence

- Limited disposable income

- Tracks every transaction religiously

- Moves banks to find better deals

- Motivated by commissions and rewards

Key hook: Loyalty points + zero-fee transactions

👩💼

Wealth Optimizer

High intent, high confidence

- Low debt, desire for financial control

- Accumulates rewards strategically

- Compares products before switching

- Needs significant value prop to move

Key hook: Savings goals + premium card features

🧑

Trust Seeker

Low intent, lower confidence

- Little to no disposable income

- Low trust in financial institutions

- Needs to see others using it first

- Barrier: significant value prop needed

Key hook: Referral incentives + social proof

🧑💻

Habit Former

Low intent, higher confidence

- Just starting out saving money

- Learning to manage finances actively

- May have unexpected or irregular debts

- Tracks spending to feel in control

Key hook: Spending insights + savings nudges

Low Financial Intent

Original internal segmentation models have been abstracted.

____________________________________________________________________________________________________________________________________________________________

DESIGN ARTIFACT 02

Mapping the gap between

download and daily use

One of the first things I did was map the actual customer journey; not the intended one, but the one customers were experiencing. What I found was a series of broken handoffs. The onboarding flow asked for effort before it demonstrated value. The chatbot escalated instead of resolving. And the transition from "new user" to "active user" was invisible; there was no designed moment where a customer felt like they had actually arrived.

The journey map became the organizing artifact for the redesign. Every friction point on the map became a brief. Every emotional low became a design opportunity.

01 DISCOVERY

02 DOWNLOAD

03 FIRST LOGIN

04 FIRST ACTION

05 DAILY BANKING

Sees ad / friend referral, checks social presence

Downloads app, starts registration, verifies identity

Opens app, sees home screen, is asked "how will you use this?"

Adds money, makes first payment or activates card

Returns daily, uses loyalty, bills, savings, refers friends

Pain Point

Messaging mismatch

Ads promise instant banking; flow feels slow and formal

KYC drop-off

Identity verification step causes high abandonment rates

Feature overload

Generic home screen shows everything at once; no clear step

First action unclear

Users don't know what to do first or why it matters

Retention cliff

No habit-building triggers after the first transaction

Opportunity

Social proof layer

Peer-to-peer referral mechanics and discovery campaigns

Progressive KYC

Show value before asking for effort; reduce form fields

Persona-aware UX

Personalization question routes user to the right first feature

Activation prompt

Contextual nudges tied to persona goal and intent

Loyalty as habit engine

Daily login streaks, points, and rewards reinforce return

____________________________________________________________________________________________________________________________________________________________

ONBOARDING REDESIGN

Replacing a generic first experience

with a persona-aware one

The old onboarding flow presented every feature at once. There was no differentiation between a new user who wanted to save money and one who wanted to pay bills. The home screen was built for the product team, not the customer. It showcased everything the app could do rather than guiding the user to the thing they should do first.

The redesign introduced a personalization gate early in the onboarding flow. A simple question that routed users to a persona-matched first experience. The question also seeded our behavioral intelligence layer, giving the data team a first signal to work with from day one.

Before

No personalization. Feature dump.

After

Intent-led. Trust-building.

Step 1

App download & install

😟

Step 2

Full KYC form upfront

No context. No value shown yet.

😵

Step 3

Generic home screen

8+ features shown at equal weight

Pay

Save

BNPL

Cards

Scan

Market

Loyalty

Bills

😕

Step 4

No clear next step

User self-navigates. Intent unknown.

📉 Drop-off. Low habit.

High abandonment. Low return usage.

Step 1

App download & install

Key Innovation

Step 2

"How will you use Reflect?"

Intent captured before anything else

💰 Save

💳 Pay

🎁 Earn

📊 Track

Routes to persona-matched experience ↓

✓

Step 3

Contextual KYC

Shorter. Purpose explained. Trust earned.

🎯

Step 4

Persona-matched home screen

Primary actions. Relevant features only.

YOUR FIRST STEP: Add money to your wallet

✨

Step 5

First action + reward moment

50 loyalty points. Positive first memory.

📈 Daily habit begins.

High completion. High return. Real banking.

____________________________________________________________________________________________________________________________________________________________

BEFORE AND AFTER

From feature showcase

to intent-driven experience

The before state of the home screen was built around what the product offered. Every feature was surfaced at equal visual weight, leaving users to figure out what to do first. There was no personalization, no designed progression, and no moment of felt value.

The redesigned experience was built around what the user came to do. The persona selection at onboarding directly informed the home screen hierarchy. Surfacing the actions most likely to match intent and routing everything else into a secondary layer.

____________________________________________________________________________________________________________________________________________________________

AI SUPPORT LAYER

Designing for resolution,

not escalation

The support experience was a symptom of the same structural problem: no system had been designed to understand what a customer actually needed before routing them. Every query, regardless of complexity, defaulted to a human agent queue; creating backlogs, slow response times, and a support load that scaled linearly with user growth. A model that would not survive expansion.

I led two parallel AI initiatives to fix this. The first was a WhatsApp-based triage chatbot built on Infobip; designed to classify intent before responding, routing routine queries to instant automated resolution and complex cases to human agents with the full conversation context pre-packaged. WhatsApp was the right channel for these customers because it was the messaging platform they were already in. The second was the integration of an in-app AI assistant, bringing transactional capability and personalized guidance directly into the product. Unlike a traditional chatbot, this AI assistant understood Arabic in colloquial form, not just formal language, through voice or text. Users could ask it to execute transfers, settle bills, or check account details conversationally.

Together, these two layers formed a complete AI support stack: Infobip handling reactive triage on WhatsApp and the AI-assistant enabling proactive, conversational banking inside the product. The design rationale across both was: a system that tries to handle everything fails at everything. Knowing scope, and handing off cleanly when something exceeds it, builds trust even in escalation.

Chatbot Triage Architecture - WhatsApp

Customer sends WhatsApp message

Received by Infobip chatbot layer

AI Intent Classification

Key Innovation: Triage before response

Routine Query

Handled by bot

Balance inquiry / account summary

Transaction status / recent history

Bill pay confirmation / card activation

Bot auto-responds

Templated answer + relevant next step

✓ Resolved - no agent needed

Escalation Trigger

Flagged for agent

Disputed / unrecognized transaction

Blocked account / fraud alert

Large transfer failure / card fraud

Priority queue + context handoff

Intent + full conversation sent to agent

✓ Triaged - agent starts informed

Abstraction of configuration, proprietary chatbot scripts, and production conversation trees.

____________________________________________________________________________________________________________________________________________________________

ECOSYSTEM AND ALIGNMENT

Building the intelligence layer

and the shared language

The work was not just about the product. A redesigned app would not hold if the rest of the organization was still optimizing for different things. I ran co-creation workshops with Marketing, Data Science, Operations, and Customer Experience to align around a single shared growth metric - "the North Star" - and establish common definitions for activation, retention, and success.

At the same time, we built out the behavioral intelligence infrastructure: funnel analytics tracking drop-off at every step of the onboarding and activation flow, cohort segmentation mapping user behavior to archetypes over time, and social signal monitoring that surfaced feedback patterns before they became volume issues.

I also advocated strongly for a design system; not only as a design team deliverable, but as organizational infrastructure. A shared component library meant faster builds, fewer production incidents from UI inconsistencies, and a common visual language that aligned design, development, and QA around the same source of truth.

____________________________________________________________________________________________________________________________________________________________

IMPACT

Outcomes measured over

a six-month period

📱

+~20%

Onboarding completion rate

After the onboarding experience redesign, more users were completing registration and reaching their first active state.

🤖

+40%

Chatbot resolution rate

After restructuring the support conversation flows, customers self-resolved faster and escalation rates dropped.

💰

4x

Cash-in trajectory

Total cash-in grew from $2.4M to $11.4M as more users completed the first transaction and built deposit habits.

⚡

2x

Feature adoption

By routing users to the right feature at the right moment, adoption doubled across key product areas.

🔧

200+

Production incidents resolved

The experience overhaul - including design system adoption and improved QA processes - cleared a significant backlog of incidents.

👥

+125K

Active accounts

Active status defined by internal KPI measuring spending behavior and business-aligned engagement goals.